What Is Full Coverage Car Insurance? (And What It Doesn't Cover)

If you’ve ever shopped for a car loan, asked an agent for a quote, or read the fine print on a lease, you’ve heard the phrase “full coverage.” It sounds reassuring. It sounds like everything is taken care of. And that’s exactly the problem.

Here at Coverall Insurance in New Braunfels, we talk to Texas Hill Country drivers every week who believe they’re completely protected because they have “full coverage” — only to discover after a wreck that a big piece was missing. So let’s clear this up once and for all.

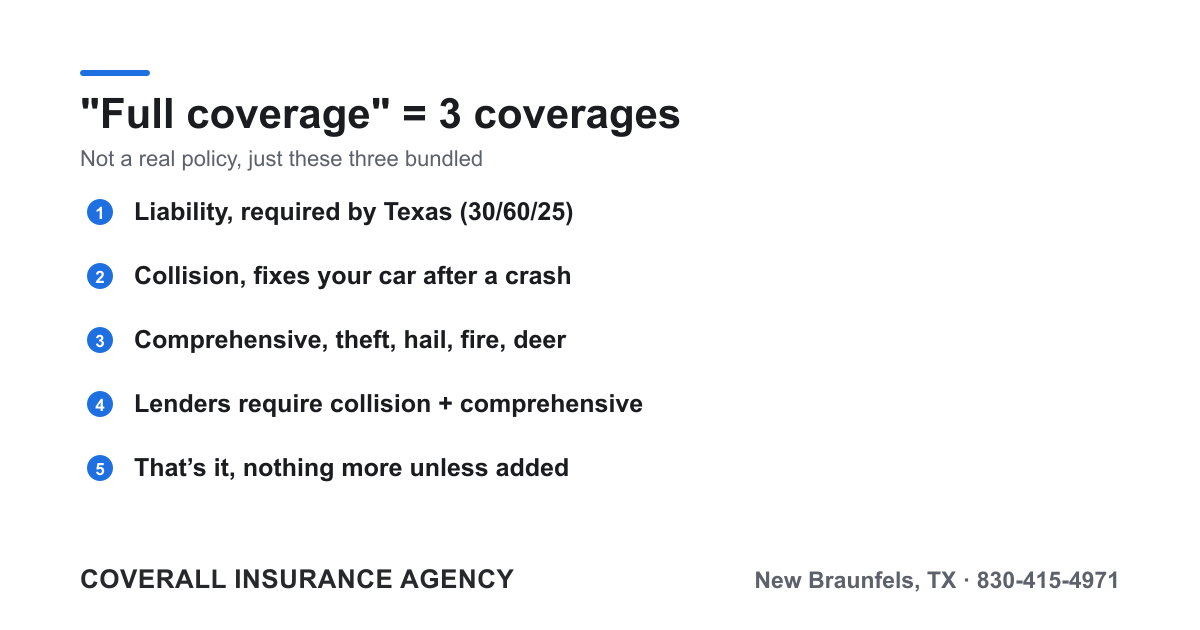

”Full coverage” is not a real policy

Here’s the most important thing to understand: “full coverage” is not an actual type of insurance, and it’s not a legal term. You can’t buy a policy called “full coverage.” No statute defines it. No insurer sells it as a single product.

It’s marketing shorthand — an informal phrase the industry uses to describe a policy that bundles together three separate coverages:

- Liability coverage — pays for the other person’s injuries and property damage when you cause an accident

- Collision coverage — pays to repair or replace your car after a crash, no matter who’s at fault

- Comprehensive coverage — pays for damage to your car from things other than a collision: theft, hail, fire, vandalism, flooding, or hitting a deer on a dark Hill Country road

When you put those three together, people call it “full coverage.” But the name promises far more than the policy actually delivers. Full coverage does not mean everything is covered. It means you have those three building blocks — and nothing more unless you specifically added it.

To see how these pieces fit into a complete policy, take a look at our overview of standard auto insurance.

What full coverage actually includes

Let’s break down the three core parts.

1. Liability (required by Texas law). Texas requires every driver to carry minimum liability limits of 30/60/25 — that’s $30,000 for injuries per person, $60,000 per accident, and $25,000 for property damage. Liability is the only legally mandated coverage. It protects other people, not you or your car.

2. Collision. This pays to fix your own vehicle after an accident — whether you rear-ended someone, slid on wet pavement, or got hit by an at-fault driver who turns out to be uninsured. You’ll have a deductible (commonly $500 or $1,000) that you pay before coverage kicks in.

3. Comprehensive. Often called “other than collision,” this handles the non-crash stuff: a tree limb falling on your hood, a hailstorm rolling through Comal County, a stolen car, or a windshield cracked by gravel on the highway.

That’s it. That’s “full coverage.” Three coverages — one required, two optional.

Why lenders require collision and comprehensive

If you financed or leased your car, you’ve almost certainly been told you need “full coverage.” Here’s why.

When you take out a loan, the bank or lender technically owns part of your car until it’s paid off. They’re protecting their investment. If your car gets totaled or stolen, they want to be sure the loss is paid for — so they require you to carry both collision and comprehensive until the loan is satisfied.

Liability alone won’t cut it for a lender, because liability never pays for your vehicle. So the “full coverage” requirement isn’t really about protecting you — it’s about protecting the lender’s money. Once your car is paid off, that requirement disappears, and the choice to keep collision and comprehensive becomes yours.

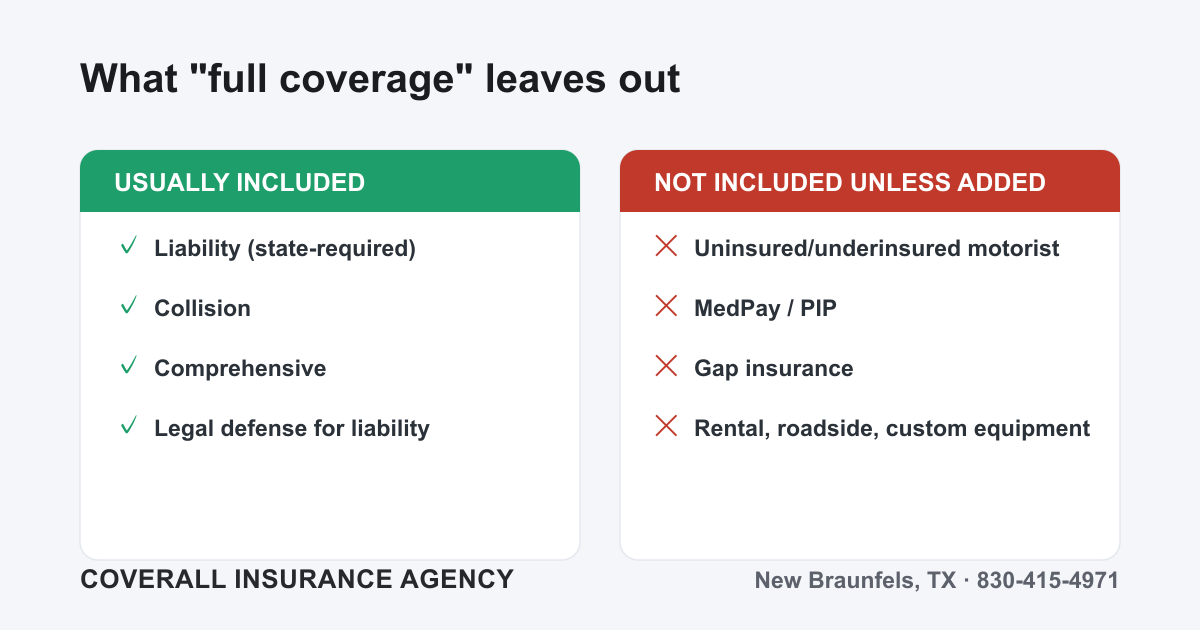

What “full coverage” does NOT include

This is the section the big insurance brands tend to gloss over. “Full coverage” leaves out a surprising number of things that drivers assume are baked in. Unless you specifically added them, the following are usually not part of your policy:

- Uninsured/Underinsured Motorist (UM/UIM) — If a driver with no insurance (or not enough) hits you, this is what pays for your injuries and car. Roughly one in five Texas drivers is uninsured, which makes this one of the most important coverages to add. Learn more in our guide to uninsured and underinsured motorist coverage in Texas.

- Medical Payments (MedPay) / Personal Injury Protection (PIP) — Covers medical bills for you and your passengers regardless of fault. PIP can even help with lost wages. In Texas this is optional and frequently skipped.

- Gap insurance — If your financed car is totaled, your insurer pays its current market value — which is often less than what you still owe. Gap insurance covers that difference so you’re not paying off a loan on a car you no longer have.

- Rental reimbursement — Pays for a rental car while yours is in the shop after a covered claim. Without it, you’re renting out of pocket.

- Roadside assistance — Towing, jump-starts, lockouts, and flat-tire help are add-ons, not automatic.

- Custom equipment coverage — Aftermarket wheels, lift kits, stereo systems, and other upgrades aren’t covered beyond a small default limit unless you schedule them.

On top of those add-ons, “full coverage” never covers normal wear and tear, mechanical breakdowns, intentional damage, personal belongings stolen from inside the car, or using your personal vehicle for business without proper commercial coverage.

The false sense of security

The real danger of the phrase “full coverage” is psychological. People hear “full” and stop asking questions. They assume the gaps above are filled. Then a wreck happens, an uninsured driver speeds off, and they learn — too late — that “full” never meant “complete.”

We’ve seen drivers with so-called full coverage stuck with thousands in medical bills, a loan balance on a totaled car, and no rental to get to work. The policy did exactly what it was designed to do. It just wasn’t designed to do everything the name implied.

A smarter approach is to ignore the label and ask: What am I actually trying to protect — my health, my car, my savings, my family? Then build coverage to match. For larger families or higher-net-worth households, it’s also worth layering on a personal umbrella policy for liability protection that goes beyond standard auto limits.

If you’re trying to figure out the right limits and add-ons for your situation, our guide on how much car insurance you need in Texas walks through it step by step. You can also explore all of our auto insurance options to see how the pieces fit together.

Bottom line

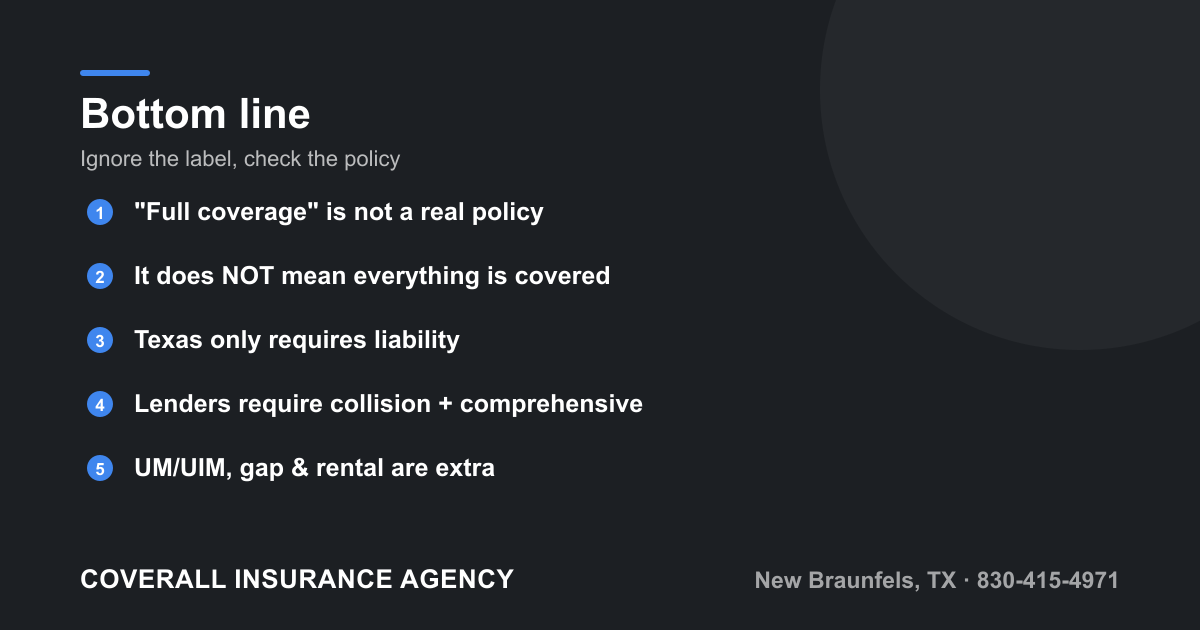

- “Full coverage” is not a real policy or a legal term — it’s marketing shorthand for liability + collision + comprehensive.

- It does not mean everything is covered.

- Texas only requires liability (30/60/25). Collision and comprehensive are optional unless a lender requires them on a financed or leased car.

- Critical protections like UM/UIM, MedPay/PIP, gap, rental, roadside, and custom equipment are not included unless you add them.

- The name creates a false sense of security — what matters is what’s actually on your policy, not what it’s nicknamed.

Don’t let a marketing term decide how protected you are. The team at Coverall Insurance in New Braunfels will review your current policy line by line, point out exactly where the gaps are, and shop multiple carriers to fit your budget and your life in the Texas Hill Country.

Get a free auto insurance quote or policy review today — contact us here or call 830-415-4971.