Why You Need Uninsured/Underinsured Motorist Coverage in Texas

You buy auto insurance to protect yourself on the road. But here’s a hard truth a lot of Texas drivers never learn until it’s too late: your liability coverage doesn’t pay for your injuries. It pays for the other person’s. So what happens when the driver who hits you has no insurance at all, or just barely enough to cover a fender bender? That’s where uninsured/underinsured motorist coverage steps in, and in Texas, it’s one of the most important coverages you can carry.

The problem: too many Texas drivers aren’t insured (or barely are)

Texas has a serious uninsured-driver problem. Industry estimates put roughly 1 in 5 vehicles on Texas roads as uninsured or underinsured, with millions of registered vehicles not matched to an active insurance policy. On top of that, plenty of drivers who are insured carry only the state minimum liability limits of 30/60/25:

- $30,000 for bodily injury per person

- $60,000 for bodily injury per accident

- $25,000 for property damage

That sounds like a lot until you’re the one in the hospital. A single ambulance ride, an ER visit, an MRI, and a short stay can blow past $30,000 fast. A serious crash with surgery, physical therapy, and lost wages can easily run six figures. If the at-fault driver only carries $30,000 and you have $120,000 in injuries, where does the other $90,000 come from? Not from their policy. And not from your own liability coverage either.

What UM/UIM actually covers

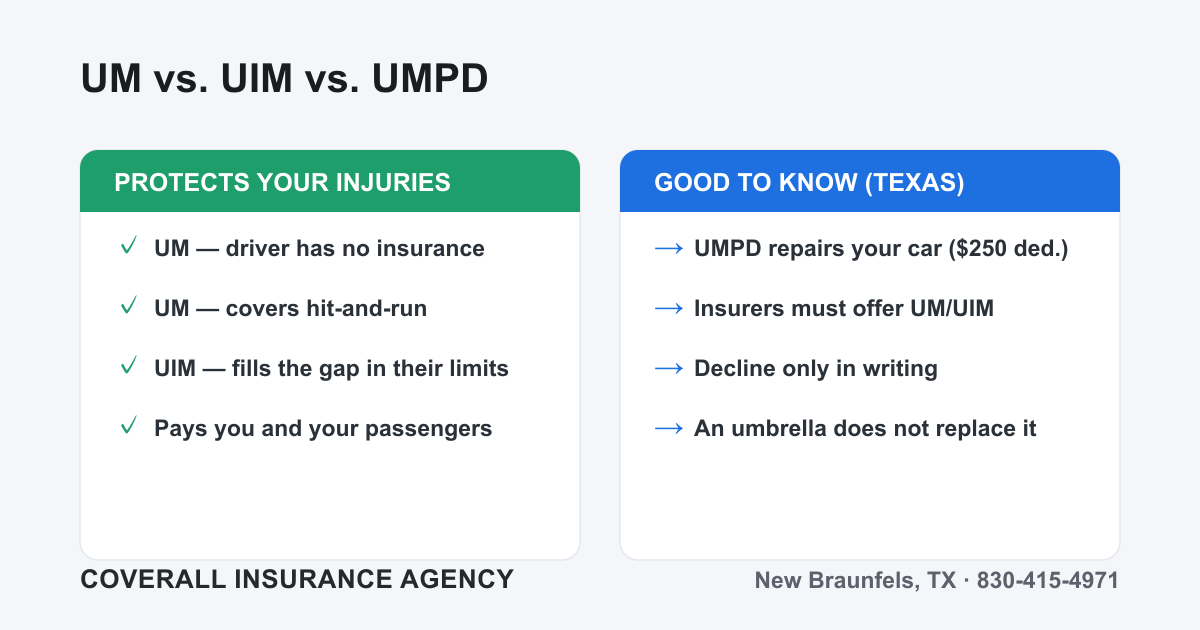

Uninsured/underinsured motorist coverage protects you and your passengers when someone else causes a crash and can’t pay for the harm they caused. There are two situations it handles, and the difference matters:

- Uninsured Motorist (UM): The at-fault driver has no insurance at all, or it’s a hit-and-run where the driver can’t be identified. Your UM coverage steps in as if it were their policy.

- Underinsured Motorist (UIM): The at-fault driver has insurance, but not enough. Their limits get exhausted, and your UIM coverage picks up the remaining gap, up to your own UIM limit.

Within both, there are two parts:

- Bodily Injury (UM/UIM BI): Pays for medical bills, lost wages, pain and suffering, and long-term care for you and your passengers.

- Property Damage (UMPD): Pays to repair or replace your vehicle when the at-fault driver can’t.

This is coverage you cannot get any other way. It’s the only part of your auto policy designed to make you whole when the person who hurt you can’t.

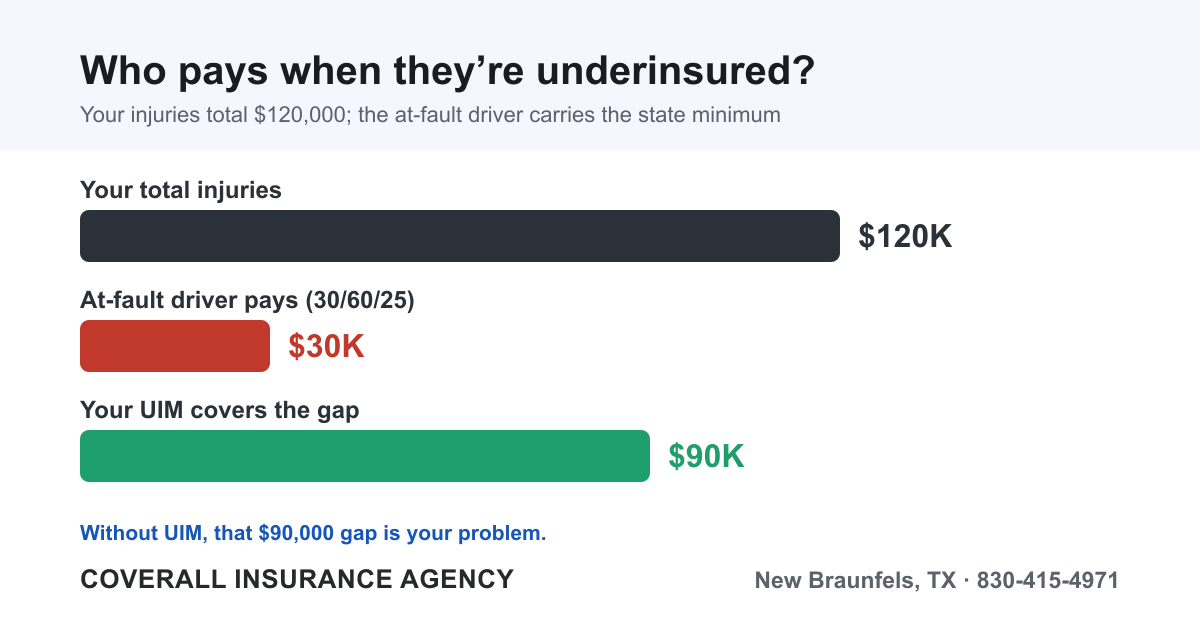

A realistic example: who pays the gap?

Let’s put real numbers on it.

You’re stopped at a light on the way home in New Braunfels. A driver rear-ends you at speed. You end up needing surgery and months of physical therapy. Your total damages — medical bills, lost wages, and pain and suffering — come to $120,000.

The at-fault driver carries the Texas minimum: $30,000 in bodily injury coverage.

- Their insurance pays the first $30,000.

- That leaves $90,000 in bills with nowhere to go.

Without UIM coverage, that $90,000 is your problem. You can sue the driver, but you can’t collect money they don’t have, and most minimum-limits drivers don’t have it.

With $100,000 in UIM coverage, your own policy pays the difference. Their $30,000 plus your UIM combines to cover the full $120,000, and you’re not stuck eating tens of thousands in medical debt for a crash that wasn’t your fault. That’s the entire point of the coverage.

UMPD vs. collision: the deductible nuance most drivers miss

Here’s something competitors rarely explain clearly. If an uninsured driver wrecks your car, you might be able to fix it two different ways: through collision coverage or through uninsured motorist property damage (UMPD). They’re not the same.

- Collision pays for your vehicle damage regardless of who’s at fault, but you pay your collision deductible (often $500 or $1,000), and a claim can affect your rates.

- UMPD in Texas covers your vehicle when an uninsured driver is at fault, and it comes with a $250 deductible by statute. That’s often lower than a typical collision deductible, and because the other driver was clearly at fault, it’s the cleaner way to handle the claim.

One catch: in Texas, UMPD generally requires that the at-fault uninsured driver be identified. For a true hit-and-run where no one knows who hit you, UMPD typically won’t pay for vehicle damage — that’s where your collision coverage becomes important. (The bodily-injury side of UM, however, still covers your injuries in a hit-and-run.) Carrying both UMPD and collision closes that gap completely.

Hit-and-run: why UM matters even when you never find the driver

A driver sideswipes you on I-35 and takes off. You never get a plate. Their “insurance” can’t help you because there’s no one to bill. Uninsured motorist bodily injury coverage treats a hit-and-run like an uninsured-driver crash, so your medical bills and injuries are still covered. Without UM, a hit-and-run can leave you paying out of pocket for an accident you did nothing to cause.

Texas law: insurers must offer it, and you can only decline it in writing

UM/UIM coverage is not mandatory in Texas, but the law builds in a safeguard. Texas requires insurers to offer you UM/UIM coverage when you buy a policy. You can only turn it down by rejecting it in writing.

What does that mean for you?

- If you never signed a written rejection, you may already have this coverage — check your declarations page.

- If you did decline it, it was a choice you may not even remember making. It’s worth revisiting.

For more on how this fits into your overall policy, see our guides to standard auto insurance and how much car insurance you really need in Texas.

Doesn’t my umbrella policy cover this? Not quite.

A common misconception: “I have a personal umbrella, so I’m covered.” A personal umbrella policy is excellent for extending your liability limits — the coverage that protects you when you injure someone else. But a small or standard umbrella typically does not add UM/UIM protection unless you specifically buy an endorsement for it, and that endorsement usually requires you to carry meaningful UM/UIM limits on your underlying auto policy first.

In other words: an umbrella protects your assets when you’re at fault. UM/UIM protects your body and your bank account when someone else is at fault and can’t pay. They solve different problems, and you generally want both. Stacking strong UM/UIM under an umbrella is how you build real protection.

How much UM/UIM should you carry?

A good rule of thumb is to match your UM/UIM limits to your liability limits, and to carry more than the state minimum. Common, sensible options include $100,000/$300,000 for bodily injury, with higher limits available if you have assets or income to protect. The premium is often surprisingly affordable, because it only pays out when the other driver fails to. To dial in the right amount, start with our auto insurance overview or talk it through with an agent.

Bottom line

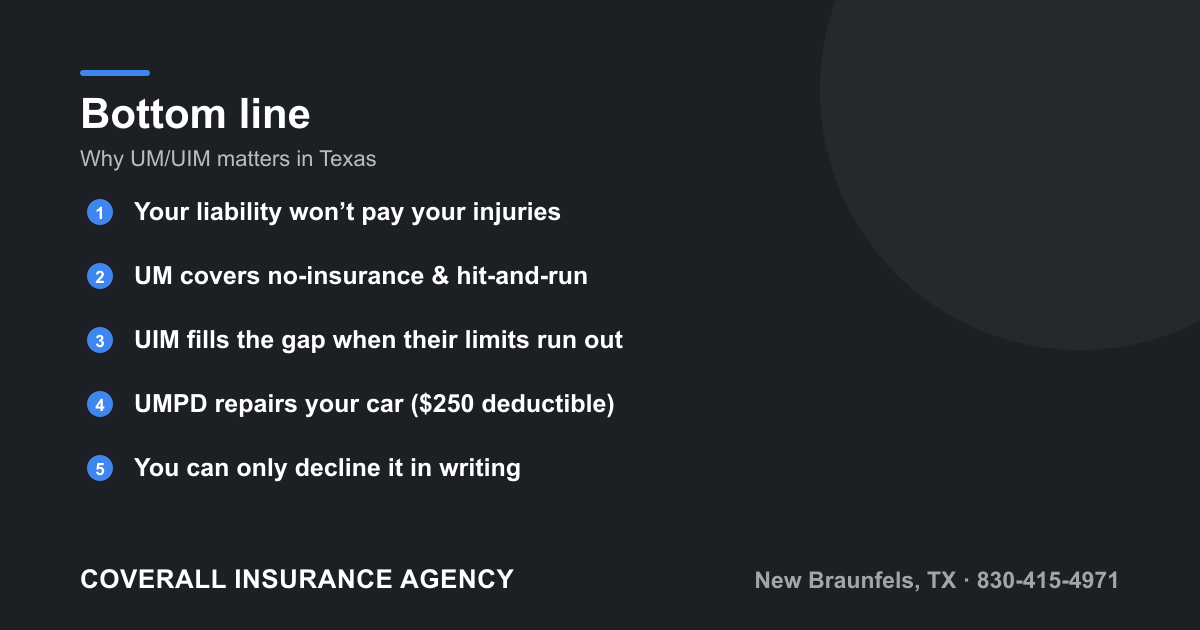

You can be the safest, most responsible driver in the Hill Country and still get hurt by someone who isn’t insured, isn’t insured enough, or doesn’t stick around. Your liability coverage won’t help you in that moment, because it was never designed to.

- UM covers you when the at-fault driver has no insurance or flees the scene.

- UIM covers the gap when their limits run out and yours don’t.

- UMPD ($250 deductible in Texas) handles your vehicle when an identified uninsured driver is at fault; collision backs you up for hit-and-runs.

- Texas insurers must offer it, and you can only decline it in writing — so check your policy.

- An umbrella extends liability, not your own injury protection — you want both.

UM/UIM coverage is one of the smartest, most affordable ways to protect yourself, your family, and your finances from a risk that’s entirely out of your control.

Not sure whether you have UM/UIM, or how much? Coverall Insurance Agency in New Braunfels will review your current policy and find the right coverage for you. Get a free auto insurance quote or policy review or call 830-415-4971 today.