Replacement Cost vs. Actual Cash Value Roof Insurance: What Texas Homeowners Need to Know

If you own a home or commercial building in the Texas Hill Country, the single most important line in your insurance policy might be how it pays for your roof. After a hailstorm, two neighbors with nearly identical roofs can get wildly different checks from their insurers, and the reason almost always comes down to two letters: RCV or ACV.

Here in hail country, this is not a small distinction. It can be the difference between a fully covered new roof and a check that barely dents the bill. Let’s break down exactly how each one works, where the depreciation traps hide, and what to check on your own policy before the next storm rolls through.

RCV vs. ACV: the core difference

Replacement Cost Value (RCV) pays what it costs to replace your damaged roof today, with materials of similar kind and quality, minus only your deductible. No deduction for age. No deduction for wear.

Actual Cash Value (ACV) starts with that same replacement cost, then subtracts depreciation based on the roof’s age and remaining useful life. You get the “used” value of the roof, not the cost to rebuild it new.

That depreciation subtraction is the whole ballgame, and it punishes roofs more than almost any other part of your property. A roof has a predictable lifespan (a typical asphalt shingle roof is often modeled at 20 to 25 years), so insurers depreciate it on a steady schedule. A 15-year-old roof can be considered 60% to 75% “used up” before a single shingle is even inspected.

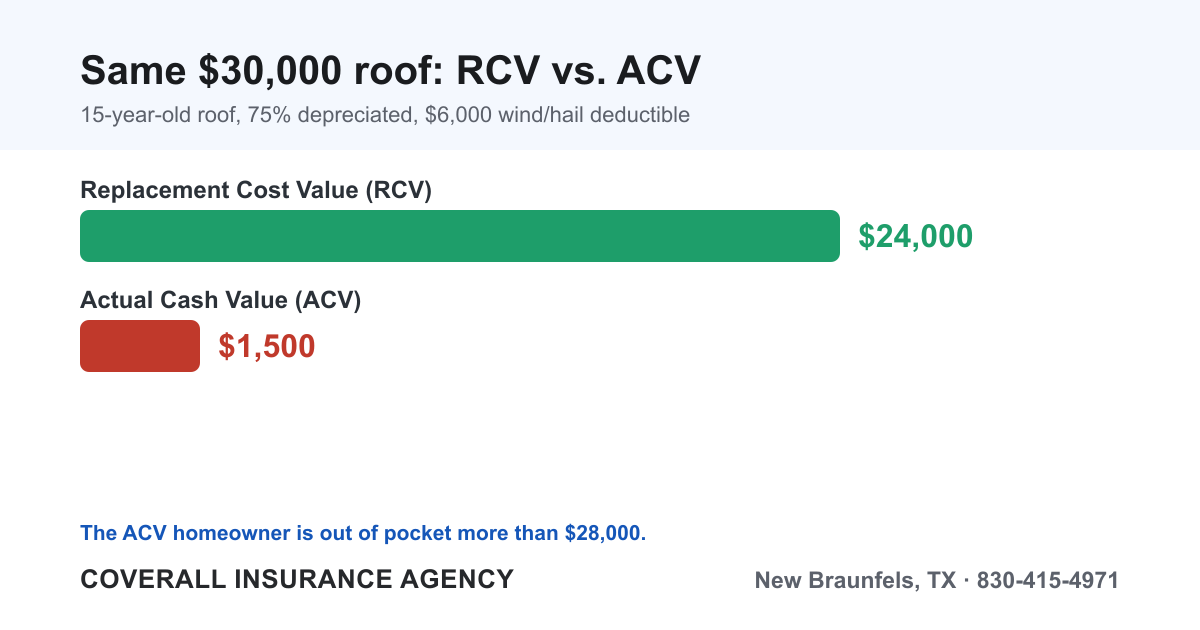

A worked dollar example: $30,000 roof

Say a hailstorm destroys your roof, and the replacement cost is $30,000. Your wind/hail deductible is 2% of a $300,000 dwelling, or $6,000. The roof is 15 years old on a 20-year depreciation schedule, so it’s 75% depreciated.

Under RCV coverage:

- Replacement cost: $30,000

- Minus deductible: -$6,000

- You receive: $24,000 (paid in two stages — more on that below)

Under ACV coverage:

- Replacement cost: $30,000

- Minus 75% depreciation: -$22,500

- Depreciated (ACV) value: $7,500

- Minus deductible: -$6,000

- You receive: $1,500

Same storm. Same roof. Same $30,000 bill. The ACV homeowner is out of pocket more than $28,000. That is not a typo, and it is exactly why understanding your coverage type matters so much. (For more on how that 2% deductible works in Texas, see our guide to wind and hail deductibles in Texas.)

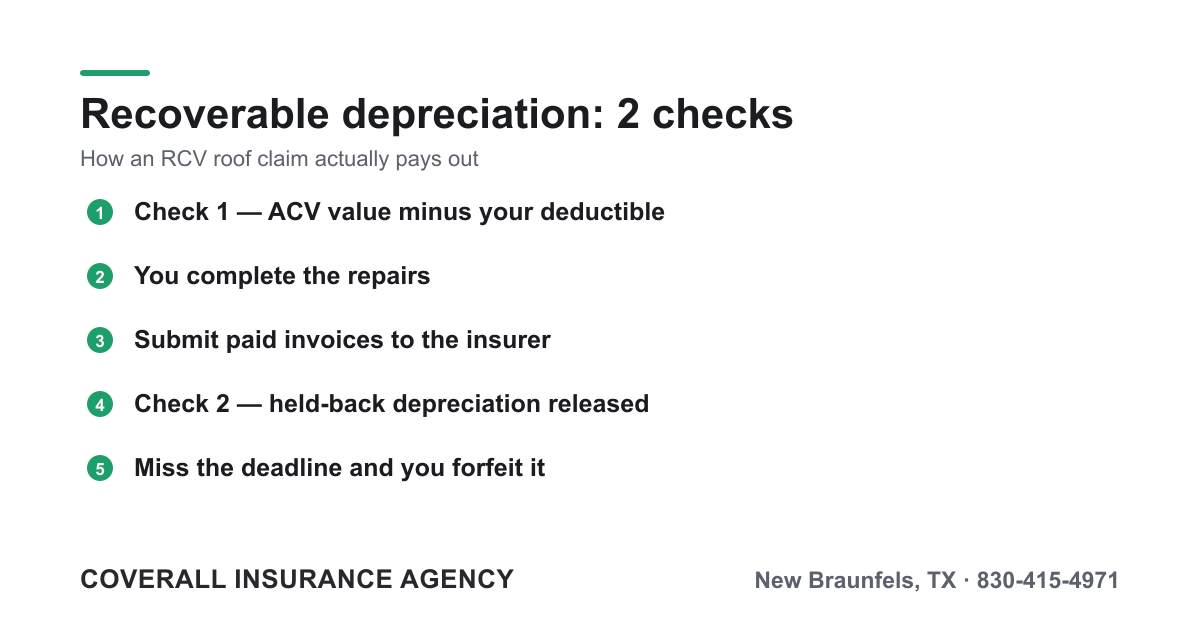

Recoverable depreciation: the part almost everyone misses

Here’s a detail most competitor articles skip entirely. Even on an RCV policy, the insurer usually doesn’t hand you the full $24,000 up front. Instead, it works in two payments:

- First check (ACV payment): The insurer pays the depreciated value minus your deductible right away. In our example, that’s the $1,500.

- Second check (recoverable depreciation): Once you actually complete the work and submit paid invoices, the insurer releases the held-back depreciation — the remaining $22,500.

This held-back amount is called recoverable depreciation, and it is only recoverable if you finish the repairs and document them. Miss the deadline (policies often give you a year or two), and that money can be lost. On a pure ACV policy, there is no second check — the depreciation is non-recoverable. What you see is what you get.

Knowing this prevents two costly mistakes: thinking your insurer “lowballed” you on the first check, and pocketing the first check without ever completing repairs.

The Texas twist: roof payment schedules and surfacing endorsements

In recent years, many Texas carriers have stopped offering full RCV on older roofs. Even if the rest of your home is insured on a replacement-cost basis, your roof may be carved out onto a separate roof payment schedule (sometimes called a roof surfacing payment schedule or roof endorsement).

These endorsements set the payout by roof age and material using a fixed table. A 15-year-old composition shingle roof might be listed at 40% of replacement cost; a 20-year-old roof at 25% or less. The schedule is printed right in your policy, so you can — and should — read it before a claim.

A few important wrinkles:

- These schedules often apply only to wind and hail losses. A fire or a falling tree may still be covered at full replacement cost.

- Roof age affects eligibility, not just payout. Many insurers won’t write or renew a policy at all if the roof is past 15 to 20 years, or they’ll require an inspection first. If you own an older property, our older home insurance page covers the workarounds.

- Mobile and manufactured homes are frequently placed on ACV roof terms by default. See our mobile home insurance guide for what to ask.

Cosmetic damage exclusions

Another quiet trap: the cosmetic damage exclusion. Common on metal roofs (and increasingly on others), this endorsement says the insurer won’t pay for hail dents that are only visual and don’t affect the roof’s function or watertightness. After a hailstorm, you could have a roof full of dimples and still get denied because the damage is deemed “cosmetic.” If you have a metal roof, look specifically for this exclusion.

Market value ≠ replacement cost

People often assume their payout is tied to what the house is worth. It isn’t. Market value includes your land, your location, and the housing market — none of which factor into rebuilding a roof.

Replacement cost is purely the cost of materials and labor to rebuild. In many Hill Country neighborhoods, replacement cost is actually higher than a portion of the market value, because land is cheap relative to construction. Your roof check is based on construction cost, full stop — not on Zillow.

Ordinance or law: don’t forget code upgrades

When an old roof is replaced, current building codes may require upgrades the original didn’t have — new decking, ice-and-water shield, upgraded fasteners, or bringing the whole structure up to current wind ratings. A standard policy may not pay for those code-driven extras.

Ordinance or law coverage fills that gap. Without it, even an RCV policyholder can be stuck paying out of pocket to satisfy the inspector. For an older home or a commercial building, this is essential — and frequently left off by default.

This applies to commercial property, too

Everything above applies to businesses as well as homes. Warehouses, retail centers, and office buildings in Texas face the same hail exposure, the same ACV-vs-RCV question, and the same roof schedules — often with even larger dollar gaps because the roofs are bigger. If you own a building, review your commercial property insurance to confirm how your roof is valued.

Bottom line: what to check on your policy

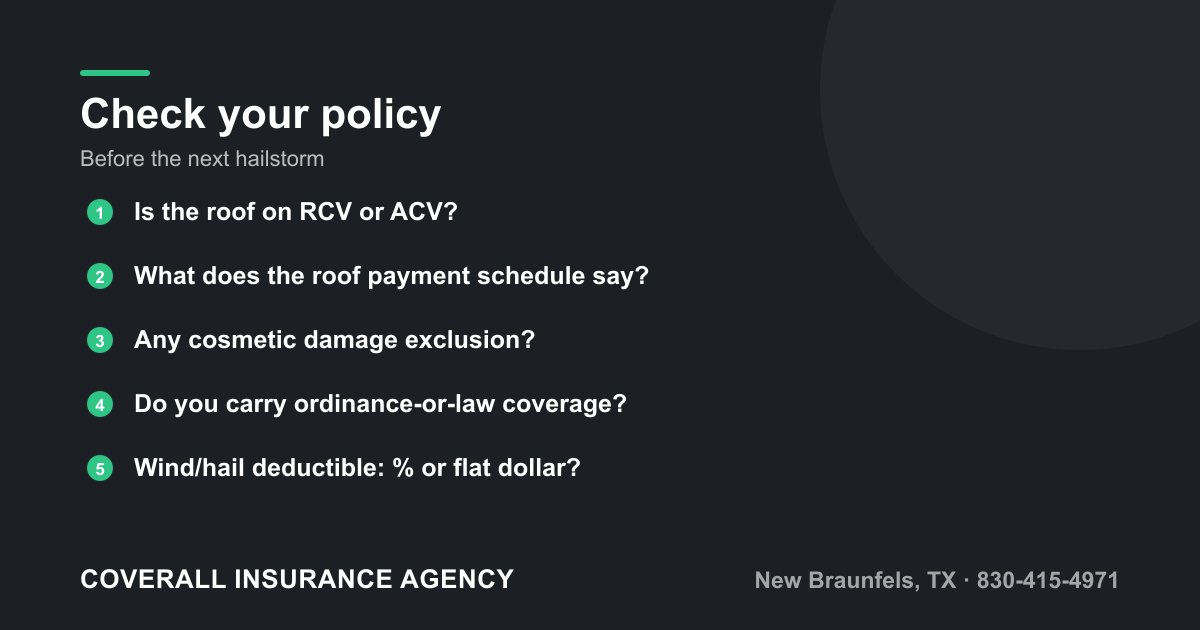

Pull out your declarations page and endorsements, and confirm:

- Is your roof on RCV or ACV? Look for “actual cash value,” “roof payment schedule,” or “roof surfacing” language.

- What does the depreciation table say for your roof’s age and material? Do the math now, not after a storm.

- Is there a cosmetic damage exclusion (especially on metal roofs)?

- Do you carry ordinance or law coverage for code upgrades?

- What’s your wind/hail deductible, and is it a percentage or a flat dollar amount?

- How old is your roof, and does it threaten renewal eligibility?

If you’re unsure on any of these, you’re not alone — these terms changed quietly on a lot of Texas renewals. When a storm hits, follow the steps in our hail damage roof guide, and make sure your underlying homeowners insurance is built to actually pay for a new roof, not a depreciated fraction of one.

Want to know exactly how your roof is covered before the next hailstorm? Coverall Insurance Agency offers a free home-insurance review — we’ll read the fine print with you and flag any ACV traps. Contact us or call 830-415-4971 today.