What Does Workers' Compensation Insurance Actually Cover? A Plain-English Guide for Texas Employers

If you employ people in the Texas Hill Country, “workers’ comp” is one of those phrases everyone uses and few people fully understand. Most articles online give you the same short list: medical bills, lost wages, maybe rehab. That’s accurate, but it leaves out the single most valuable piece of the policy for a business owner, and it skips the rules that actually decide whether you’re protected when something goes wrong.

Here’s the complete picture, in plain English.

The two halves of a workers’ comp policy

A standard workers’ compensation policy actually does two jobs, and understanding both is the key to understanding the whole product.

- Part One – Workers’ Compensation. This pays statutory benefits to an injured employee: medical care, a portion of lost wages, rehabilitation, and death benefits. The employee doesn’t have to prove the employer did anything wrong.

- Part Two – Employer’s Liability. This is the part competitors forget. It defends and pays on behalf of the business when an injury leads to a lawsuit against the company, rather than a standard benefits claim.

Most online guides describe only Part One. The real value of a workers’ compensation policy is that you get both.

What workers’ comp covers

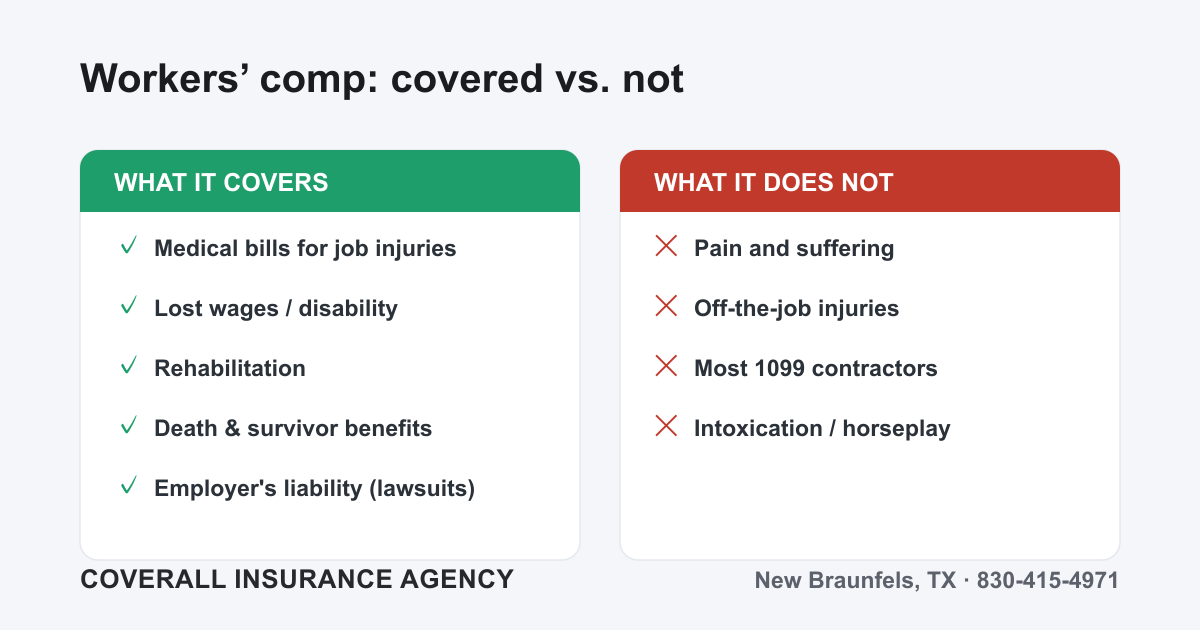

1. Medical bills for job-related injuries and illnesses

If the injury or illness arises out of and in the course of employment, the policy pays for the treatment, with no deductible or co-pay for the worker. That includes:

- Emergency care, surgery, and hospital stays

- Doctor visits, imaging, and prescriptions

- Occupational illnesses like repetitive-stress injuries (carpal tunnel), hearing loss, or chemical and dust exposure

Coverage isn’t limited to the four walls of your shop. An employee hurt while making a delivery, visiting a job site, or driving for work is generally covered too.

2. Lost wages and disability benefits

When an injury keeps someone off the job, comp replaces part of their income, typically a percentage of their average weekly wage up to a state cap. Benefits are usually categorized as:

- Temporary (the worker will recover and return)

- Permanent (lasting impairment), and either partial or total

These are wage-replacement benefits, not full salary. They’re designed to keep an injured worker afloat, not to make them whole the way a jury award might.

3. Rehabilitation

The policy pays for physical therapy, occupational therapy, and vocational rehabilitation — the care and retraining that help an employee recover and get back to productive work. For physically demanding fields like construction and manufacturing, this is often the difference between a worker returning to the trade and leaving it for good.

4. Death and survivor benefits

If a workplace injury is fatal, comp pays funeral and burial costs plus ongoing survivor benefits to a spouse and dependents. No family should face that loss and a financial cliff at the same time.

5. Employer’s liability (the part nobody talks about)

Workers’ comp generally makes benefits the exclusive remedy — meaning an employee who accepts comp benefits usually can’t also sue you for the injury. But there are gaps where a suit can still land: third-party-over actions, certain serious-injury claims, or a spouse’s loss-of-consortium claim. Employer’s liability coverage pays your legal defense and any judgment in those situations. It’s the reason a comp policy protects the company, not just the employee.

What workers’ comp does NOT cover

This is where business owners get surprised. Workers’ comp is broad, but it is not unlimited.

- Pain and suffering. Comp pays defined economic benefits only. There’s no jury-style award for emotional distress or “punitive” damages — that trade-off is the whole point of the exclusive-remedy bargain.

- Off-the-job injuries. Get hurt at home, on vacation, or during your commute, and it’s generally not covered.

- Most independent contractors (1099). Comp covers employees, not true independent contractors. Misclassifying workers is a common and costly mistake — if a “contractor” really functions as an employee, you can be on the hook anyway.

- Injuries from intoxication, horseplay, fighting, or intentional self-harm. Drugs, alcohol, goofing around, or deliberately hurting yourself will typically void a claim.

The details that decide your coverage and your premium

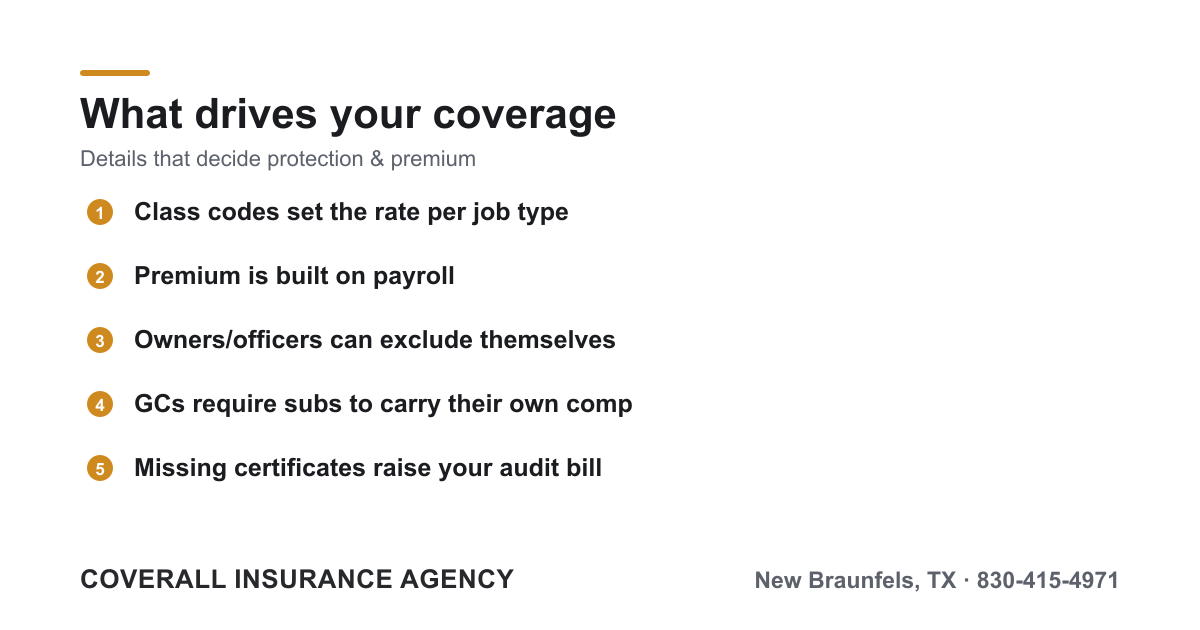

General contractors require subs to carry their own comp

On a job site, certificates of insurance (COIs) matter. A general contractor will almost always require subcontractors to carry their own workers’ comp and provide a certificate proving it. If a sub’s uninsured worker gets hurt, that injury can roll up onto your policy — and your premium — at audit. This is everyday reality in construction, where one missing certificate can cost real money.

Owner and officer exclusions

Sole proprietors, partners, and corporate officers can often elect not to cover themselves under the policy, which lowers premium. That can make sense if you carry strong personal health and disability coverage, but it also means you have no comp benefits if you’re injured. It’s a decision worth making on purpose, not by accident.

Class codes and payroll drive your premium

Comp pricing isn’t random. Each type of work gets a class code with its own rate (a roofer’s code costs far more than a clerical one), and your premium is built on payroll within each code. Accurate class codes and clean payroll records keep your audit fair — misreporting in either direction comes back to bite you.

The Texas twist: subscriber vs. non-subscriber

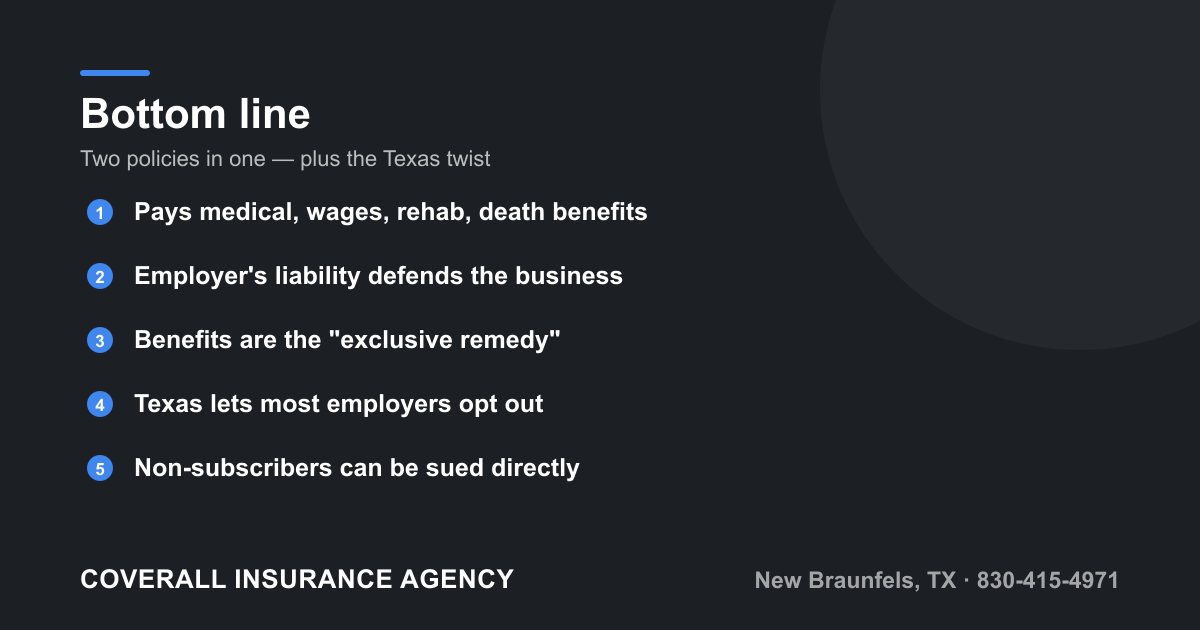

Here’s what makes Texas different from nearly every other state. Texas does not require most private employers to carry workers’ comp. Employers can “opt out” and become non-subscribers.

That freedom comes with a serious catch: a non-subscriber loses the exclusive-remedy protection and can be sued directly by an injured employee, often without the legal defenses other employers enjoy. Some businesses choose this path with a carefully built alternative plan; many regret it after the first lawsuit. Because this decision is so consequential for Texas employers, we cover it in depth in our guide to Texas workers’ comp subscriber vs. non-subscriber rules. Read it before you decide to go without coverage.

Bottom line

Workers’ compensation covers medical care, lost wages, rehabilitation, and death benefits for job-related injuries, and just as importantly, it provides employer’s liability coverage that defends your business when an injury turns into a lawsuit. It does not pay for pain and suffering, off-the-job injuries, most 1099 contractors, or injuries from intoxication and horseplay.

In Texas, you may technically be allowed to skip it, but opting out trades a predictable premium for unpredictable lawsuits. For most employers, carrying comp is the cleaner, safer choice. The right setup depends on your class codes, payroll, owner elections, and whether you hire subs.

Want it dialed in for your business? Get a business insurance quote through our intake form or call us at 830-415-4971. As an independent agency in New Braunfels, we’ll compare carriers and build a policy that fits how you actually operate — and you can always reach out with questions first.