Does Umbrella Insurance Cover Everything? The Myth That Trips Up Most Texans

Ask ten people what umbrella insurance does, and most will tell you some version of the same thing: “It’s the policy that covers everything my other insurance doesn’t.” It’s a comforting idea. It’s also wrong — and that misunderstanding is one of the most common (and most expensive) mistakes we see at our New Braunfels office.

A personal umbrella policy is one of the best values in all of insurance. But it does one specific job extremely well, and it is not a catch-all safety net that patches every hole in your coverage. Let’s clear this up once and for all, because the difference between what people think an umbrella does and what it actually does can leave you badly exposed at the worst possible moment.

What an umbrella policy actually does

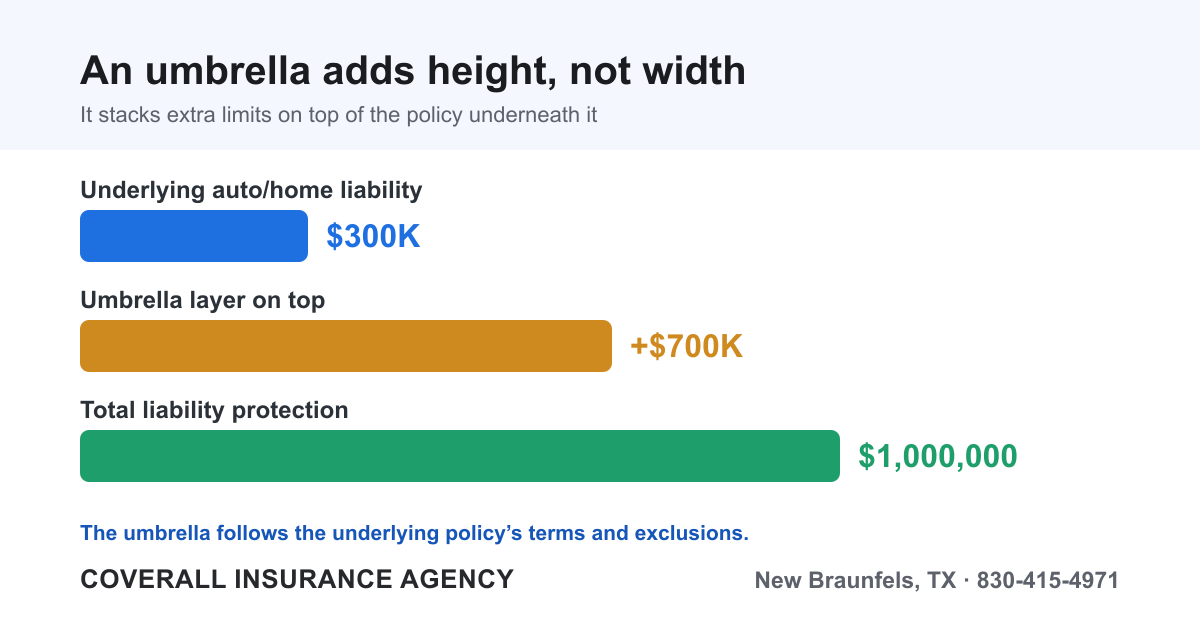

Here is the single most important sentence in this whole article: an umbrella policy adds additional liability limits on top of your underlying auto, home, or business liability coverage — and nothing more.

That’s it. It is extra liability protection, stacked above your existing policies. If you carry $300,000 in liability on your auto insurance and you cause an accident that results in a $1 million judgment against you, your auto policy pays its $300,000, and a $1 million umbrella picks up the remaining $700,000.

Two things to understand about how this works:

- It only kicks in after your underlying limits are exhausted. The umbrella sits on top; your home or auto policy pays first.

- It follows the underlying policy. This is the part everyone misses. The umbrella generally adopts the same terms, definitions, and exclusions as the policy beneath it. If your auto policy covers a type of claim, the umbrella extends more limit for that claim. If your auto policy excludes something, the umbrella almost always excludes it too.

That last point is the whole ballgame. An umbrella does not broaden your coverage. It does not fill coverage gaps. It adds height, not width.

The big myth: “it covers what my other policies miss”

Many websites — including some big-name carriers — blur this line. You’ll read that umbrella insurance “may cover claim types your base policies exclude.” That phrasing creates a dangerous impression: that the umbrella is a gap-filler.

In reality, for the vast majority of situations, the rule is simple: if the underlying policy excludes it, the umbrella excludes it too. A personal umbrella is fundamentally an excess liability policy. Its purpose is to give you more dollars of protection for the same kinds of liability claims your home and auto already cover — not to insure new categories of risk.

So if you were relying on your umbrella to cover something your homeowners policy specifically leaves out, you may be in for a very unpleasant surprise after a claim. The fix for a coverage gap is usually a better or broader underlying policy — or an endorsement — not an umbrella sitting on top of the gap.

What an umbrella does NOT cover

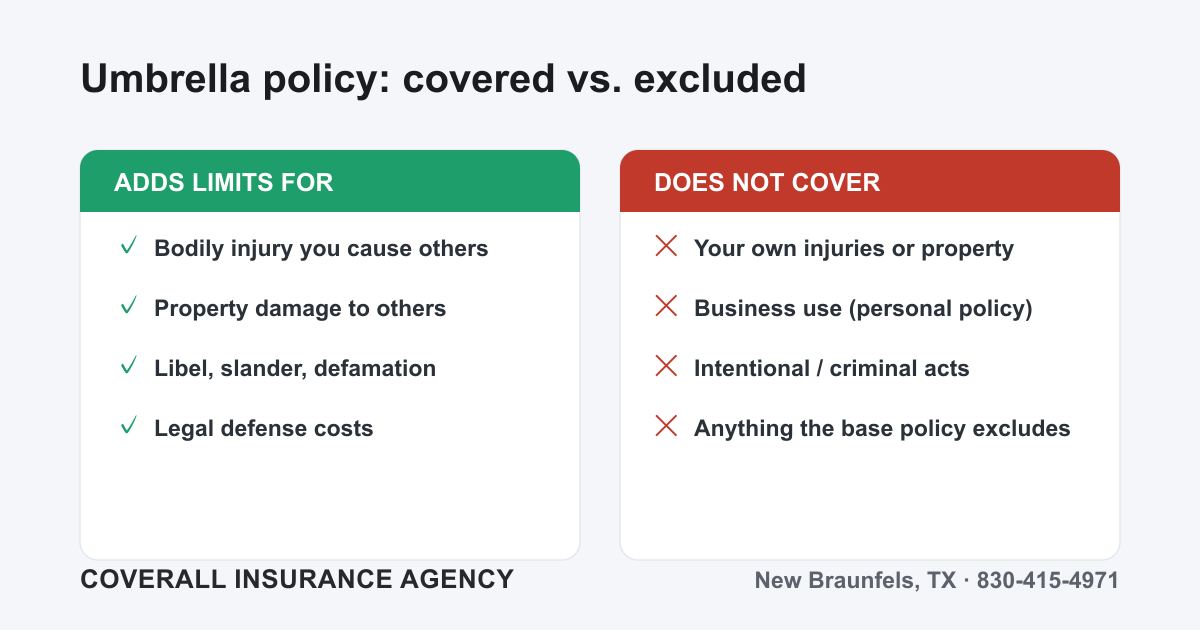

Because it’s pure third-party liability protection, an umbrella leaves out a lot of things people assume are included:

- Your own injuries. If you get hurt, that’s a first-party loss — handled by your health insurance, auto med-pay, or PIP, not your umbrella.

- Your own property. Damage to your house, your car, or your belongings is never an umbrella claim. That’s what your home insurance and auto physical-damage coverage are for.

- Business activities on a personal umbrella. This is a huge one. Liability arising from running a business — even a home-based one like in-home daycare, an Etsy side hustle, or short-term rentals — is generally excluded from a personal umbrella. If you own a business, you need a separate commercial umbrella policy.

- Intentional or criminal acts. Deliberately causing harm is never covered. Umbrellas (like all liability insurance) respond to accidents and negligence, not intent.

- Professional services. Errors, omissions, or malpractice from your profession need professional liability (E&O) coverage, not an umbrella.

- Contractual liability. Obligations you take on by signing a contract are typically excluded.

- War, and in many policies, family-versus-family claims. Injuries one household member causes another are often excluded too.

Notice the through-line: the umbrella protects you when you are legally liable to someone else for bodily injury or property damage. It is not there to make you whole for your own losses.

What it DOES cover (and covers well)

When it’s the right tool, it’s a fantastic one. A personal umbrella typically extends your liability limits for:

- Bodily injury you cause others — the at-fault car wreck, the guest injured on your property.

- Property damage you cause others.

- Certain personal-injury offenses like libel, slander, and defamation — coverage many base policies don’t include much of.

- Legal defense costs, which the umbrella often pays in addition to your limit. A defense alone can cost tens of thousands of dollars.

For most Hill Country families with a home, a couple of vehicles, a pool, a teen driver, or any visible assets, $1 million in extra protection often costs only a couple hundred dollars a year. We break down who genuinely benefits in Do You Need a Personal Umbrella Policy?.

The requirement most articles forget: minimum underlying limits

Here’s the detail almost every competitor glosses over — and it matters a lot. An umbrella can’t float on its own. It requires you to carry minimum liability limits on the policies underneath it.

Carriers do this on purpose. The umbrella is designed to attach above a solid foundation, so they require that foundation to be high enough. Typical requirements look like:

- Auto: often $250,000/$500,000 bodily injury (or $300,000 combined) plus property damage.

- Home/renters: often $300,000 in personal liability.

- Boats, ATVs, rental properties: their own minimums, depending on the carrier.

If your underlying limits drop below those required minimums — say you let your auto liability lapse to the state floor — there’s a gap between your policy and the umbrella that you are responsible for. Some umbrellas also carry a self-insured retention (a kind of deductible) for the rare claims not covered by any underlying policy. These are the nuts and bolts that turn an umbrella from a vague “extra coverage” into a structure that actually protects you, and it’s exactly the kind of thing an independent agent should be checking for you.

Personal vs. commercial: don’t mix them up

Because business liability is excluded from personal umbrellas, the right structure depends on the risk. Personal exposures — your family, your home, your cars — belong under a personal umbrella. Business exposures — your operations, employees, commercial vehicles, and premises — belong under a commercial umbrella that sits over your general liability, commercial auto, and (often) employer’s liability. Trying to cover a business with a personal umbrella is one of the fastest ways to discover, mid-claim, that you weren’t covered at all.

Bottom line

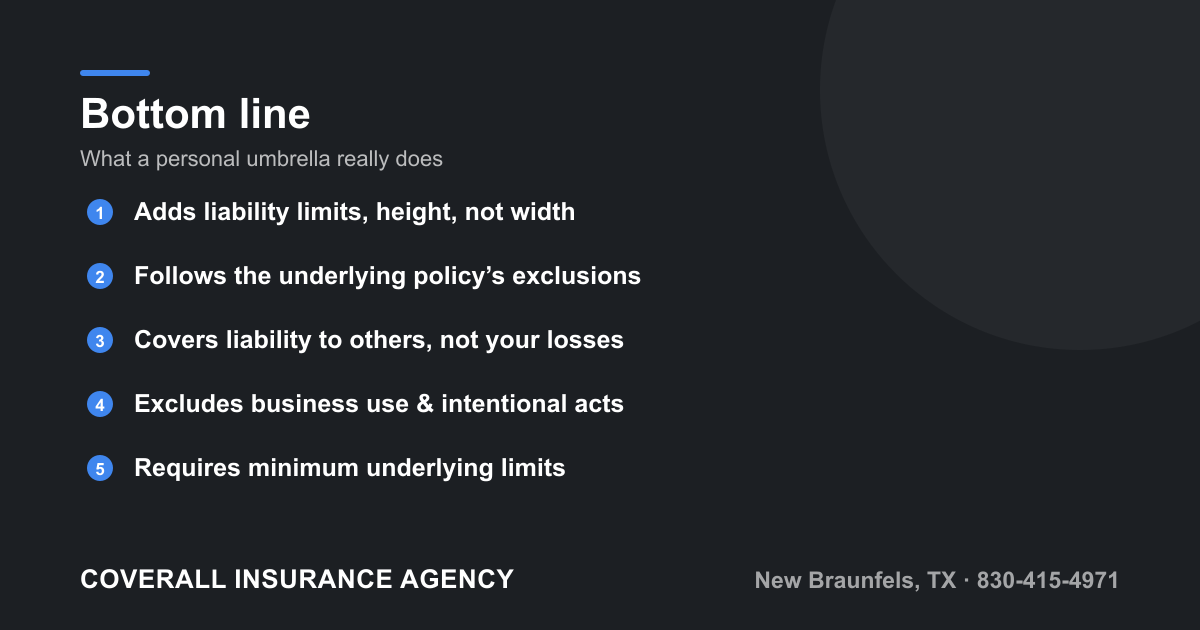

An umbrella policy is not a magic blanket that covers everything your other policies miss. Keep these truths in mind:

- It adds additional liability limits — height, not width.

- It follows your underlying policy’s terms and exclusions. If the policy below it excludes something, the umbrella generally does too.

- It covers your liability to others, never your own injuries or property.

- It excludes business activities (on a personal policy), intentional acts, professional services, and contractual liability.

- It requires minimum underlying limits to sit on top of.

Used correctly, it’s one of the smartest, most affordable layers of protection you can buy. Used as a misunderstood gap-filler, it’s a recipe for a nasty shock after a claim. The goal isn’t just to have an umbrella — it’s to build the underlying coverage correctly so the umbrella actually does its job.

Want to know whether an umbrella makes sense for you — and whether your current home and auto limits are even high enough to support one? Let’s take a look together. Request a free, no-pressure quote or call our New Braunfels team at 830-415-4971. We’ll review your real exposures, make sure the foundation is solid, and help you protect what you’ve built across the Texas Hill Country.