Does General Liability Insurance Cover Construction Defects? What Texas Contractors Need to Know

Ask ten contractors whether their general liability policy covers construction defects, and you’ll get ten different answers. It’s one of the most misunderstood topics in the trades, and the confusion is costly. Some contractors assume their general liability insurance works like a warranty that will pay to fix any callback. Others have been told it covers “nothing” related to defects. Both are wrong.

The honest answer is: it depends on what the defect damaged. General liability (GL) is built to protect you from claims that you injured someone or damaged someone else’s property. It is generally not designed to pay for tearing out and redoing your own faulty work. But there’s important nuance in between, and getting it wrong can leave you exposed on a six-figure claim.

Let’s break it down in plain English.

What general liability insurance actually covers

A standard Commercial General Liability (CGL) policy responds to third-party bodily injury and property damage caused by an “occurrence” (an accident). In a construction context, that classically means:

- Bodily injury to third parties — a homeowner trips over your extension cord, or a passerby is hurt by falling material. (Note: injuries to your own employees are handled by workers’ compensation insurance, not GL.)

- Damage to property that isn’t your work — your crew puts a forklift through the client’s existing brick wall, or a plumbing mistake floods the homeowner’s finished basement and ruins their furniture.

- Products-completed operations — claims that arise after you’ve finished the job and left the site, when your completed work allegedly causes injury or property damage down the road.

That last category is where a lot of the defect confusion lives, so it deserves its own section.

What GL covers vs. what it doesn’t

Here’s the distinction every contractor should tattoo on their estimating clipboard:

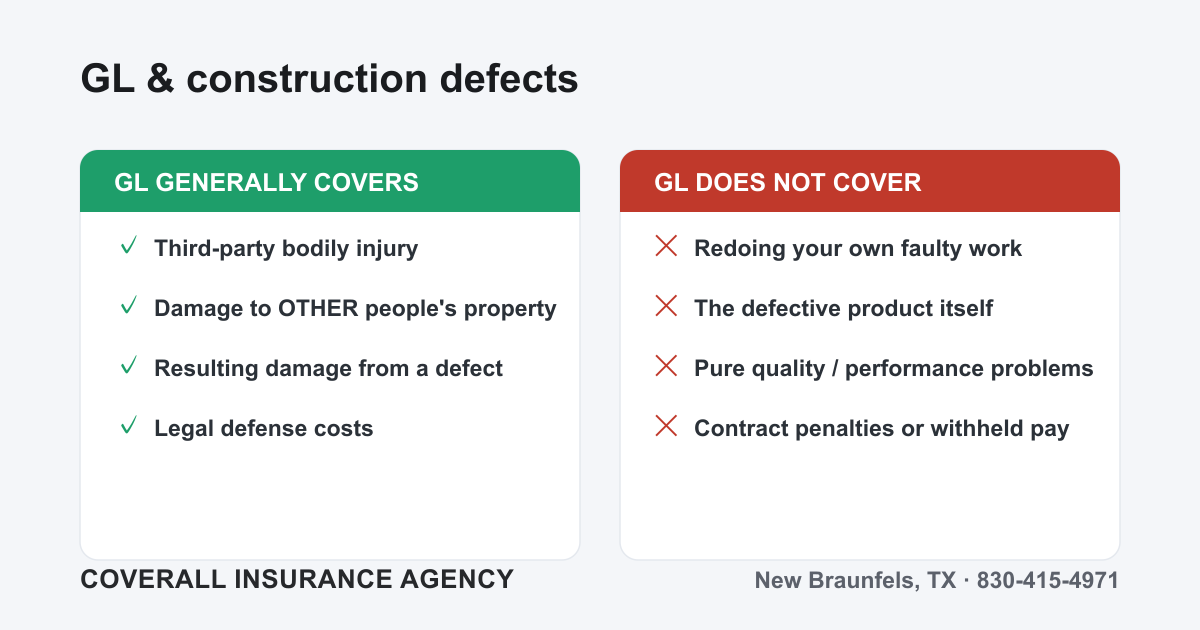

GL generally COVERS:

- Bodily injury to clients, visitors, or the public

- Damage your work causes to other property — property that isn’t the thing you built or installed

- “Resulting damage” — when a defect in your work damages something beyond the defective component itself (more on this below)

- Legal defense costs when you’re sued for a covered claim

GL generally does NOT cover:

- The cost to rip out and redo your own defective work — the bad weld, the leaking joint, the out-of-spec pour

- The repair or replacement of the faulty product or installation itself

- Pure quality or performance problems (the work simply isn’t good enough, but nothing was damaged)

- Contractual penalties, liquidated damages, or a client withholding payment

The mechanism behind those exclusions is worth understanding, because it’s where the misconceptions start.

The “your work” and faulty-workmanship exclusions

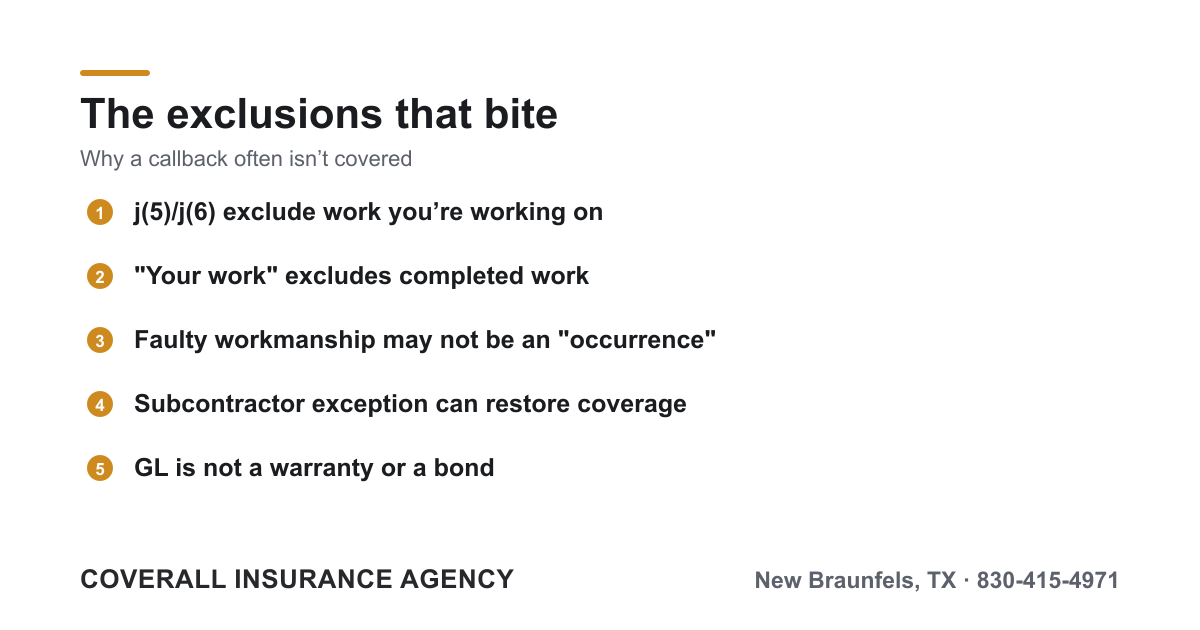

Standard CGL policies contain a series of business-risk exclusions, usually labeled j(5), j(6), and the “your work” exclusion. In broad terms:

- The j(5) and j(6) exclusions knock out damage to property you’re currently working on and to work that was done incorrectly and needs to be restored or repaired.

- The “your work” exclusion removes coverage for property damage to your completed work when the damage arises out of that work.

The logic insurers use is straightforward: GL is not a warranty, and it’s not a performance bond. Insurers don’t want to guarantee the quality of your craftsmanship — that’s a business risk you control through skill, supervision, and quality checks. If your tile job is simply bad, that’s on you, not your insurer.

This is exactly where so many contractors get blindsided. They expect a callback to be “covered,” but a callback to fix substandard work is precisely what these exclusions exclude.

The important nuance: resulting damage

Here’s the part competitors often gloss over. The exclusions target your defective work itself — not necessarily everything around it.

Example: You install a roof and a flashing detail is defective. Two things can happen:

- Replacing the bad flashing — your own faulty work. Typically excluded.

- Water intrusion ruins the drywall, insulation, and hardwood floors below — damage to other property caused by your defect. This “resulting damage” can sometimes be covered, often under products-completed operations.

So a single defect can produce both an uncovered cost (fixing your work) and a covered cost (the damage that work caused to the rest of the structure). Whether the resulting damage is actually paid still depends on the policy form, endorsements, and — critically — your state’s law.

The “occurrence” debate and why state law matters

For any of this to trigger coverage, the damage usually has to result from an “occurrence” — defined as an accident. Courts across the country have split badly on a single question: Is faulty workmanship an “accident” at all?

- Some courts say defective work is a foreseeable business risk, not an accident, so there’s no occurrence and no coverage.

- Other courts say that when faulty work causes unexpected property damage, that damage is accidental and can qualify.

This isn’t a settled question — it varies by jurisdiction and continues to evolve. The practical takeaway for a construction business: never assume a defect claim is covered or excluded based on a friend’s experience in another state. Have your specific policy and scenario reviewed.

The subcontractor exception

One of the most valuable wrinkles in the modern CGL form is the subcontractor exception to the “your work” exclusion.

In simplified terms: damage to your completed work is excluded unless the work that caused the damage was performed by a subcontractor on your behalf. For general contractors who rely heavily on subs, this exception can restore meaningful coverage for defect-related property damage that a sub caused.

The catch: this coverage can be stripped out by endorsement, and it depends on your subs actually being subs (properly insured, with you named as additional insured). Subcontractor defects are one of the biggest hidden exposures in construction insurance — verify your policy hasn’t had the exception removed, and make sure your subcontractor agreements require their own coverage.

What GL won’t do — and what fills the gap

Because GL stops well short of guaranteeing your work, contractors often layer in other protection:

- Surety bonds — A performance bond or contract bond is what actually guarantees you’ll complete the job to spec. If a client wants assurance the work will be finished correctly, that’s a bond, not a liability policy. The two are frequently confused.

- Higher limits via an umbrella — A large defect-related property-damage claim can blow through your GL limits. A commercial umbrella policy sits on top for catastrophic claims.

- Workers’ compensation — Again, GL won’t touch injuries to your own employees; that’s workers’ comp.

- Professional liability — If you do any design-build work, errors in design (versus construction) usually fall outside GL entirely.

Bottom line

General liability is essential coverage, but it is not a quality guarantee for your own work:

- It covers third-party injury and damage to other people’s property — including, sometimes, the resulting damage your defect causes to the rest of a structure.

- It does not cover the cost to rebuild your own faulty work; the j(5), j(6), and “your work” exclusions take that off the table.

- The gray areas — resulting damage, the “occurrence” debate, and the subcontractor exception — are highly fact-specific and state-dependent, so don’t rely on rumor.

- For guaranteed completion, you need a surety bond, not GL.

The worst time to learn where your coverage ends is in the middle of a defect lawsuit. An independent agent can read your actual policy language, check whether the subcontractor exception is intact, and right-size your limits.

Ready to make sure your construction business is properly protected? Get a business quote through our quick intake form, contact our team with questions, or call us at 830-415-4971. We’ll help you understand exactly what your policy covers before you need it.