Commercial Auto vs. Personal Auto Insurance: When You Actually Need a Commercial Policy

Most drivers in the Texas Hill Country assume their personal auto policy follows them everywhere a steering wheel goes. It doesn’t. The single most expensive misunderstanding we see at our New Braunfels office is a business owner or 1099 contractor who used a personal vehicle for work, had a wreck, and discovered after the fact that their claim was denied — leaving them personally on the hook for a totaled truck, the other driver’s medical bills, and a lawsuit.

This guide cuts through the marketing fluff and tells you exactly where the line is, where the gray areas hide, and how to avoid the financial gut-punch of an uncovered loss.

The core difference nobody explains clearly

Both policies pay for liability, collision, and damage. The difference isn’t what they cover — it’s when.

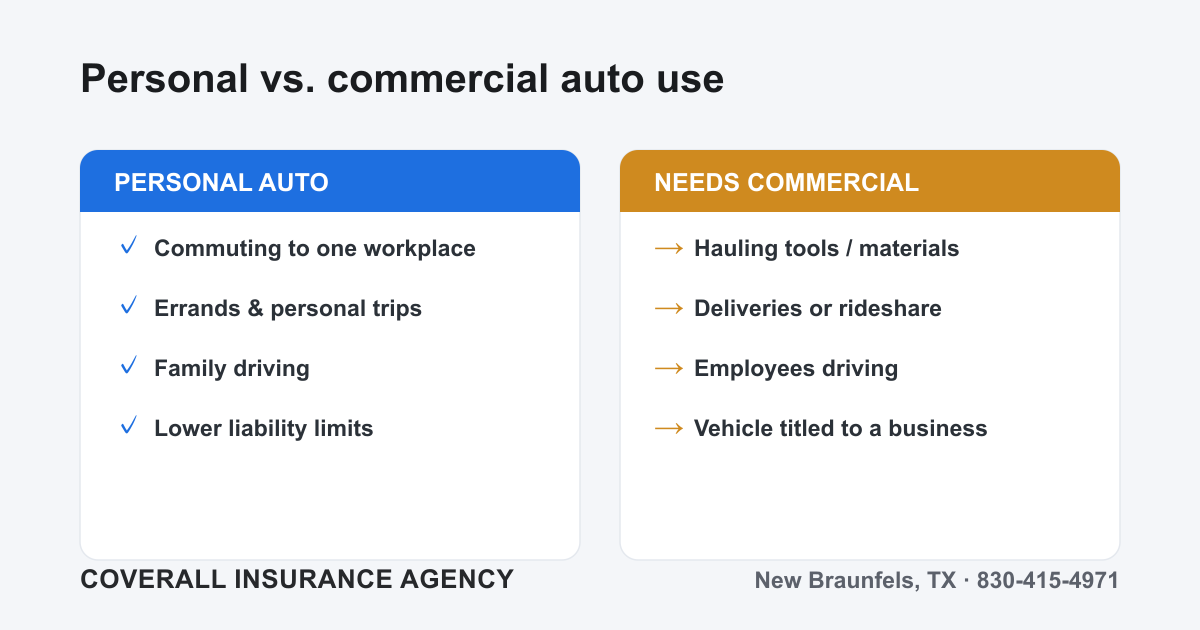

- Personal auto insurance covers you for personal use: commuting, errands, road trips, hauling the kids to school.

- Commercial auto insurance covers vehicles used to run a business — and is built for the higher risk, higher mileage, and higher liability that business driving creates.

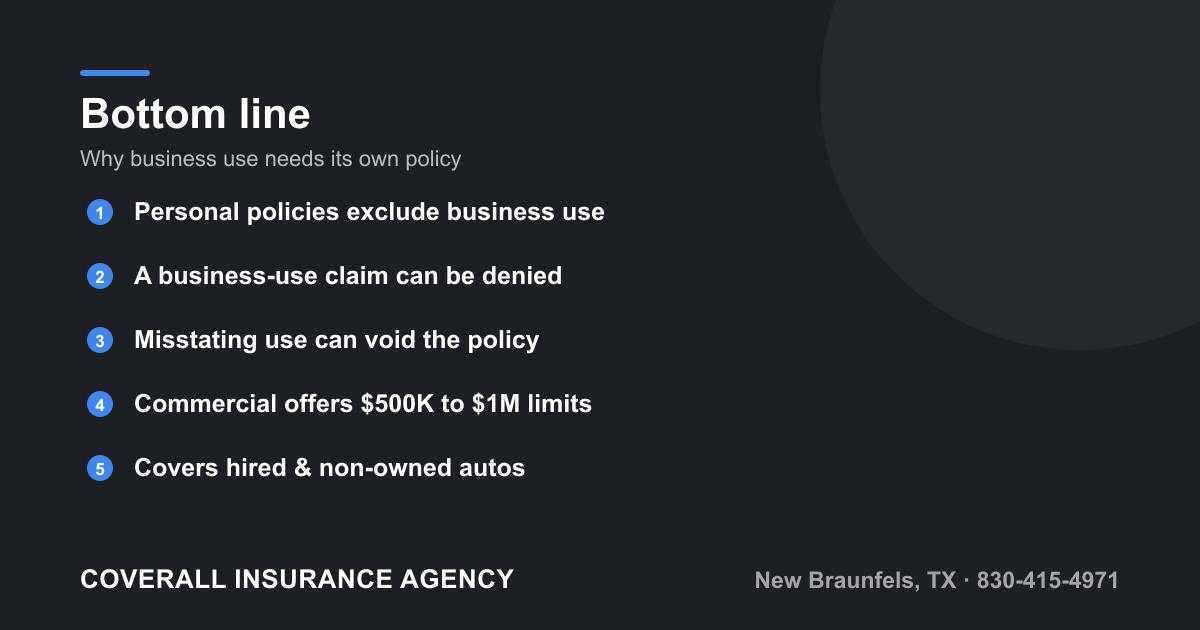

Here’s the part competitors gloss over: a personal policy doesn’t just fail to cover business use — it contains an explicit business-use exclusion. If the carrier determines the vehicle was being used “in the business or occupation of the insured” at the time of the accident, they can deny the claim outright. Worse, if you described the vehicle as “personal use only” on your application when it was really a work truck, that’s material misrepresentation — grounds for the carrier to void the policy entirely and refund your premiums instead of paying the loss.

Translation: you can pay every premium on time for ten years and still get nothing when it matters most.

When a personal policy quietly stops protecting you

Commuting to a single, fixed workplace is fine. The problems start the moment the vehicle becomes a tool of the trade. Watch for these triggers:

- Hauling tools, materials, or equipment to job sites (huge for trades — see construction).

- Making deliveries — food, packages, flowers, parts, anything for pay.

- Rideshare or driving clients/customers for a fee.

- Visiting multiple job sites or customer locations in a day as part of the work itself.

- Transporting goods for sale or carrying a meaningful business load.

- The vehicle is titled or registered to your business (more on this below).

- Employees driving the vehicle as part of their job.

If any of these describe your week, you’ve likely outgrown a personal policy. A dedicated commercial auto policy is the fix.

The gray areas that trip people up

The contractor with a personal truck

This is the classic Hill Country mistake. A plumber, electrician, framer, or landscaper buys a nice F-250, insures it personally, and drives it to job sites loaded with gear every day. They feel like they’re just driving their truck. But a claims adjuster sees a work vehicle, ladders on the rack, and a magnetic business sign on the door — and denies the claim. If you run a trade, your truck is a business asset and needs business coverage.

Deliveries and rideshare

Personal policies almost universally exclude “livery” — carrying people or goods for a fee. Driving for a delivery app or shuttling paying passengers in your personal car can void coverage for that trip. Some carriers sell a rideshare endorsement, but it’s narrow. If delivery or transport is core to what you do, you need real commercial coverage — see our transport page.

Employees driving — even their own cars

If an employee runs to the bank, picks up supplies, or makes a delivery in their own car, and they cause a wreck, the injured party will sue the deepest pocket: your business. Your employee’s personal insurer may deny it (business use), and you have no policy covering that car because you don’t own it. That gap is called hired and non-owned auto (HNOA) exposure, and almost every small business has it without realizing.

Hired & non-owned auto — the coverage competitors barely mention

Hired auto covers vehicles you rent or lease for the business. Non-owned auto covers liability when employees use their personal vehicles for company errands. Here’s the critical catch most articles skip: HNOA covers your liability to others — it does not pay to repair the employee’s personal car. It’s a liability backstop, not physical-damage coverage. For some businesses HNOA is a cheap add-on; for others, owned commercial vehicles are the answer.

Who owns and titles the vehicle?

The name on the title matters as much as how you drive.

- If the vehicle is titled to your business (an LLC, corporation, or DBA), a personal policy generally can’t even insure it correctly — the named insured is a company, not a person.

- Many owners title work trucks to the business for tax deductions and liability separation, then forget that the insurance has to match. A mismatched named insured is another fast path to a denied claim.

If your business owns the asset, the business needs the policy. Full stop.

The liability limits problem

Business driving doesn’t just change whether you’re covered — it changes how much coverage you need.

- A personal policy might carry $100,000 in liability. That sounds like plenty until a loaded work truck causes a multi-vehicle pileup with serious injuries.

- Commercial policies routinely offer limits of $500,000 or $1,000,000, and many client contracts, general contractors, and municipalities require a $1M combined single limit before you can even bid the job.

- Commercial policies also add coverages personal policies don’t: cargo, trailer/equipment, and broader hired/non-owned protection.

When a business vehicle hurts someone, the dollar figures are bigger — and so is the target on your back in a lawsuit. Underinsuring here can end a business.

Why a denied claim is so devastating

Walk through what actually happens when a personal carrier denies a business-use claim:

- Your vehicle damage — you pay out of pocket to repair or replace it.

- The other party’s property and medical bills — you pay those too.

- The lawsuit — with no insurer, you also pay your own legal defense.

- Your personal assets — home, savings, and future wages can be exposed, especially if the business isn’t properly shielded.

A $1,200/year commercial premium suddenly looks trivial next to a $250,000 judgment you’re paying yourself.

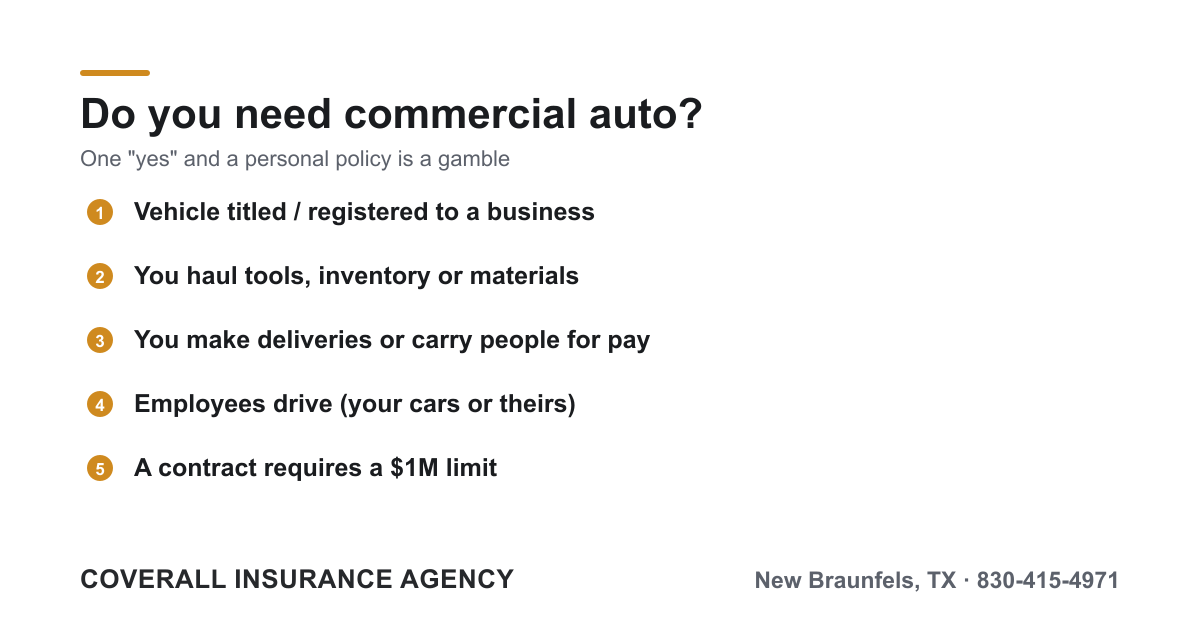

Quick gut-check: do you need commercial auto?

Answer honestly. If you say yes to even one, call us:

- Is the vehicle titled or registered to a business?

- Do you haul tools, equipment, inventory, or materials for work?

- Do you make deliveries or carry people/goods for a fee?

- Do employees drive — your vehicles or their own — on company business?

- Do you drive between multiple job sites or client locations as part of the work?

- Does a contract or client require proof of commercial auto or a $1M limit?

- Would a denied claim wipe out your business or personal finances?

One “yes” and a personal policy is a gamble you don’t want to take.

Get it right before you need it

The worst time to learn your policy doesn’t cover business use is standing on the shoulder of I-35 after a wreck. Whether you’re a contractor with one truck, an auto service shop moving customer vehicles, or a growing crew with several drivers, we’ll match your coverage to how you actually use your vehicles — no gaps, no surprises, no guesswork.

As an independent agency in New Braunfels, we shop multiple carriers to find the right fit and price for Hill Country businesses. Have a quick question first? Reach out anytime.

Ready to be properly covered? Get a business quote through our intake form or call us at 830-415-4971. A few minutes now can save your business later.